Table of Contents >> Show >> Hide

- Why Higher Mortgage Rates Cool Demand So Fast

- The Lock-In Effect Makes the Problem Worse

- Why Prices Have Not Collapsed

- Who Gets Hit the Hardest?

- Why New Construction Sometimes Looks Better Than Resales

- How Buyers and Sellers Adjust When Rates Stay High

- What It Feels Like on the Ground: Real-World Experiences in a High-Rate Market

- Conclusion

If the housing market had a catchphrase lately, it would be this: everyone wants a house, but not everyone wants that monthly payment. That, in one painfully expensive sentence, is what happens when mortgage rates climb. Buyers get pickier, sellers get twitchy, and the whole market starts moving like it forgot its coffee.

Higher mortgage rates do not just make homes more expensive in some abstract economist-with-a-spreadsheet way. They hit people where it hurts most: the monthly budget. A house that looked barely manageable when rates were low can suddenly become a “maybe after I win the lottery” situation. The result is simple and predictable. Fewer people jump in. More people wait. And the housing market loses momentum.

That is why the phrase “higher mortgage rates lead to fewer takers” is not just a headline. It is a useful summary of what happens when affordability tightens, buyer confidence fades, and would-be movers decide to sit still rather than sign up for a payment that feels like a second rent, a third job, and a mild panic attack all rolled into one.

Why Higher Mortgage Rates Cool Demand So Fast

Monthly payments rise faster than many buyers expect

Home shoppers often focus on sale price first, but mortgage rates have a sneaky way of becoming the real boss of the conversation. When rates rise, the cost of borrowing grows immediately. And because most buyers purchase based on what they can afford each month, not what looks nice in a listing photo, rising rates quickly reduce the number of people who can say yes.

Take a simple example. On a $400,000 30-year loan, a rate in the 3% range produces a dramatically lower principal-and-interest payment than a rate in the low-6% range. That difference can add hundreds of dollars a month, before property taxes, insurance, HOA fees, repairs, and the very rude surprise called closing costs. Suddenly the charming three-bedroom becomes a financial trust fall.

That payment shock matters because most households do not have unlimited flexibility. Wages do not usually jump just because mortgage rates did. So when financing costs rise, buyers either lower their budget, reduce their wish list, or step out of the market altogether.

Qualification gets tougher

Higher mortgage rates also affect who can qualify. Lenders look at debt-to-income ratios, cash reserves, credit profiles, and overall payment capacity. A higher rate can push a previously acceptable borrower over the line. That means some shoppers are not merely discouraged. They are disqualified.

This creates a filtering effect across the housing market. The most price-sensitive buyers, especially first-time buyers, get squeezed first. Move-up buyers become more cautious. Investors lose enthusiasm if financing costs eat into returns. What remains is a smaller pool of buyers with stronger incomes, larger down payments, or a willingness to compromise.

Psychology matters more than people admit

Housing is emotional, but mortgages are mathematical. Unfortunately, buyers feel both at the same time. When rates rise, many people do not just run the numbers; they compare the numbers to what they could have borrowed a year or two earlier. Even if they can still technically afford a home, the deal may feel lousy. And people hate feeling like they showed up late to the party and the chips are gone.

That psychological hesitation is powerful. Buyers start asking whether rates will fall, whether prices will soften, whether they should wait until next spring, next quarter, or the next solar eclipse. Some do move forward. Many do not. That is how higher mortgage rates create fewer takers even before the paperwork starts.

The Lock-In Effect Makes the Problem Worse

Here is where the housing market gets extra awkward. Higher mortgage rates do not only discourage buyers. They also discourage sellers.

Millions of homeowners refinanced or bought when rates were exceptionally low. For those owners, selling a home and buying another one means trading a very comfortable mortgage for a noticeably more expensive one. Even if the next home is not much pricier, the financing usually is. That reality creates what economists call the mortgage rate lock-in effect.

In plain English, people stay put because leaving would cost too much.

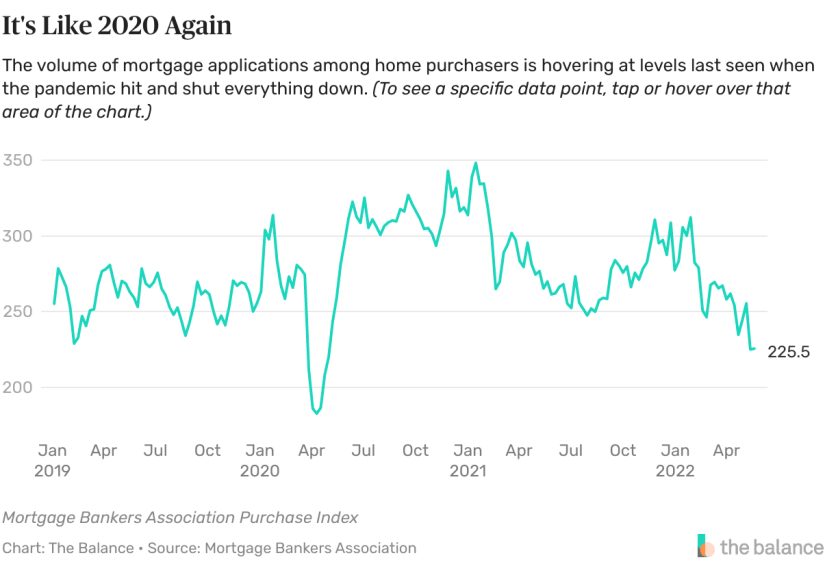

That has huge consequences. Fewer homeowners list their properties, which keeps resale inventory tight. Fewer listings mean buyers have less choice. Less choice keeps prices from falling as much as traditional affordability logic might suggest. So the market gets stuck in a strange limbo: demand is weaker, but supply is constrained too, which prevents the kind of broad price reset many frustrated buyers keep hoping for.

It is a bit like a traffic jam where everyone is annoyed, no one is moving quickly, and yet somehow the road never quite clears.

Why Prices Have Not Collapsed

At first glance, people assume higher mortgage rates should lead to sharply lower home prices. That sounds neat and tidy. Reality, as usual, is messier.

For one thing, the United States still has a long-running housing supply problem. Many markets simply do not have enough homes in the price ranges ordinary households can afford. Builders have added supply, but not enough to fully erase years of underbuilding. In many areas, especially where job growth remains healthy or land is limited, inventory is still not loose enough to cause a price free fall.

Second, sellers are not always forced sellers. Many have equity, fixed-rate mortgages, and no urgent reason to cut prices aggressively. If offers are weak, they may just wait. That keeps homes off the market and slows the downward pressure on prices.

Third, buyers adapt. They look at smaller homes, different neighborhoods, rate buydowns, adjustable-rate products, or newly built homes where builders offer incentives. So while higher mortgage rates definitely cool demand, they do not eliminate it. They simply reshape it.

The result is a market with low transaction volume rather than total collapse. In other words, fewer takers does not always mean no market. It often means a slower, choosier, more negotiated market.

Who Gets Hit the Hardest?

First-time buyers

First-time homebuyers usually feel the most pain because they are entering the market without existing home equity. They must bring cash for the down payment, closing costs, moving costs, and often emergency repairs. Add a higher mortgage rate, and the affordability cliff gets steep very quickly.

These buyers are also more likely to be balancing student loans, rent inflation, childcare costs, or limited savings. So while a higher-income repeat buyer may be annoyed by a rate increase, a first-time buyer may be knocked out of the market entirely.

Middle-income households

At the luxury end, buyers often have more flexibility or can pay cash. At the entry level, there may be support programs, family help, or smaller homes. The middle can get pinched from both directions. Prices remain too high for comfort, but incomes are not high enough to absorb the jump in financing costs without sacrifice.

Buyers in high-cost metros

In expensive cities, even a small change in mortgage rates can translate into a major monthly difference because the loan balance itself is larger. That means buyers in high-cost markets feel rate volatility with extra drama. The payment is not just higher. It is “let me stare at this calculator in silence for ten minutes” higher.

Why New Construction Sometimes Looks Better Than Resales

One of the most interesting side effects of higher mortgage rates is that homebuilders can sometimes compete better than existing-home sellers. Builders have tools individual sellers usually do not. They can offer mortgage rate buydowns, design credits, closing-cost assistance, or price cuts on inventory homes.

That makes new construction more attractive in a high-rate environment. A buyer comparing an older resale home with zero incentives against a new home with financing help may decide the new build is the better monthly deal, even if the sticker price is not lower.

Of course, builders face pressure too. Higher rates hurt affordability, slow traffic, and make financing more difficult across the industry. But compared with a regular homeowner selling one house, builders have more levers to pull. That is why new homes often capture attention when resale markets feel frozen.

How Buyers and Sellers Adjust When Rates Stay High

Buyers become more strategic

When rates are elevated, serious buyers tend to behave differently. They shop smaller, negotiate harder, compare loan products more carefully, and think more about total monthly cost than granite countertops or dramatic foyer ceilings. They also become much more willing to ask for concessions.

In a strange way, this can be healthy. The market becomes less frenzied and a little more rational. Buyers take time. Sellers have to price realistically. Agents actually have to explain things. Imagine that.

Sellers have to reset expectations

High-rate markets punish wishful pricing. Sellers who list as though it is still the ultralow-rate boom often discover that buyers are not ignoring the house because of bad luck. They are ignoring it because the math no longer works.

That does not mean every seller must slash the price. But it does mean presentation, pricing, and concessions matter much more. In a market with fewer takers, a home must look right, feel right, and pencil out right.

Everyone watches the Federal Reserve, even when they should not overdo it

Many consumers assume mortgage rates move in lockstep with the Federal Reserve. The real relationship is more complicated. Mortgage rates are influenced by inflation expectations, Treasury yields, bond markets, lender margins, and broader economic sentiment. So even when people expect relief, it may arrive slowly or unevenly.

That uncertainty itself changes behavior. Buyers wait. Sellers hesitate. Lenders market flexibility. And housing economists spend a lot of time explaining that “slightly better” is not the same thing as “cheap again.”

What It Feels Like on the Ground: Real-World Experiences in a High-Rate Market

To understand why higher mortgage rates lead to fewer takers, it helps to move beyond charts and imagine the actual people behind the numbers.

Picture a young couple who spent two years saving for a down payment while rent kept climbing. They finally feel ready to buy, open a mortgage calculator, and realize the kind of home they wanted now comes with a payment several hundred dollars above what they expected. They do not stop wanting a home. They stop feeling safe saying yes. So they delay, renew the lease, and tell themselves they are being patient. Really, they are being priced into caution.

Now picture a family that already owns a home. They need more space. Maybe a new baby is on the way, maybe a parent is moving in, maybe working from home turned the dining room into a permanent office. In a normal market, they would list and move. But their current mortgage rate is wonderfully low, and replacing it with a much higher rate makes the upgrade feel punishing. So they renovate the basement, buy bunk beds, and try to convince themselves that “cozy” is a personality trait.

Then there is the first-time buyer who keeps losing not because someone else offered more, but because the monthly payment keeps changing before they are emotionally ready to commit. One week rates dip and hope returns. The next week they bounce higher and the same house suddenly feels irresponsible. That kind of volatility wears people down. Even qualified buyers can become reluctant buyers when financing costs feel unstable.

Real estate agents feel it too. In hotter years, buyers rushed. In a high-rate market, they hesitate, circle back, recheck numbers, call the lender again, and ask whether buying down the rate makes sense. Sellers who would once have received fast offers now hear uncomfortable advice about pricing, staging, or offering concessions. Deals happen, but they often require more patience and more realism than before.

Lenders see another side of the experience. Borrowers ask sharper questions. Should they lock now? Float? Choose a temporary buydown? Consider an adjustable-rate mortgage? Wait six months? Refinance later? The tone is less “How fast can we close?” and more “Can someone please explain why this payment looks like a car loan married a tuition bill?”

Builders, meanwhile, have learned to market monthly affordability instead of just square footage. A lower rate through a buydown can matter more to shoppers than upgraded fixtures. In other words, buyers are not only shopping for homes. They are shopping for a payment they can live with.

All of these experiences point to the same truth: higher mortgage rates do not erase housing demand, but they do make every housing decision heavier. People second-guess more. They compromise more. They postpone more. That is why fewer takers show up. Not because the desire to own disappears, but because the cost of acting on that desire becomes harder to justify in everyday life.

Conclusion

Higher mortgage rates lead to fewer takers because they strike at the heart of affordability. They raise monthly payments, reduce purchasing power, tighten qualification standards, and make buyers more cautious. At the same time, they lock many current owners into place, which keeps supply constrained and prevents the kind of broad price drop that might otherwise restore balance.

That leaves the housing market in a slower, more selective phase. Homes still sell. Buyers still buy. Builders still build. But the easy momentum disappears. Every deal requires more math, more negotiation, and more patience.

The good news is that housing markets do adapt. Buyers adjust expectations, sellers become more realistic, lenders create new financing options, and builders lean on incentives. But until borrowing costs feel more manageable on a broad scale, the headline will keep writing itself: when mortgage rates stay high, the crowd gets thinner.