Table of Contents >> Show >> Hide

- “Normal” Is the Wrong Word for Markets

- Averages Hide the Mess (Returns, Valuations, and Reality)

- Volatility Isn’t a BugIt’s the Cover Charge

- If “Normal” Is Rare, What Should Investors Do?

- The “Missing Best Days” Trap (a.k.a. Timing Is Expensive)

- Specific Examples of “Not Normal” That Are Actually Normal

- A Practical Playbook for When Markets Feel Weird

- Investor Experiences: What “Normal” Really Feels Like (Extra Perspective)

- Conclusion: Normal Markets Are RareGood Plans Aren’t

If you’ve ever looked at your portfolio and thought, “Is the market broken?”congrats. You’re experiencing something extremely normal:

markets refusing to act “normal.”

Here’s the awkward truth investors learn the hard way: the market doesn’t spend much time behaving like the neat, average-filled charts in a textbook.

It lurches, sprints, naps, panics, celebrates, and occasionally does all of that before lunch. What feels abnormal is often just the market being the market.

“Normal” Is the Wrong Word for Markets

People love averages because averages are comforting. A long-term average stock return sounds like a promise, a warm blanket, and a financial plan all in one.

But markets don’t glide along at the average. They overshoot it, undershoot it, and generally treat it like a speed limit sign on an empty highway.

A “normal market” implies stability: valuations hanging around typical levels, returns clustering neatly around the long-term mean,

and interest rates politely staying in their lane. In real life, those things are raresometimes shockingly rare.

Averages Hide the Mess (Returns, Valuations, and Reality)

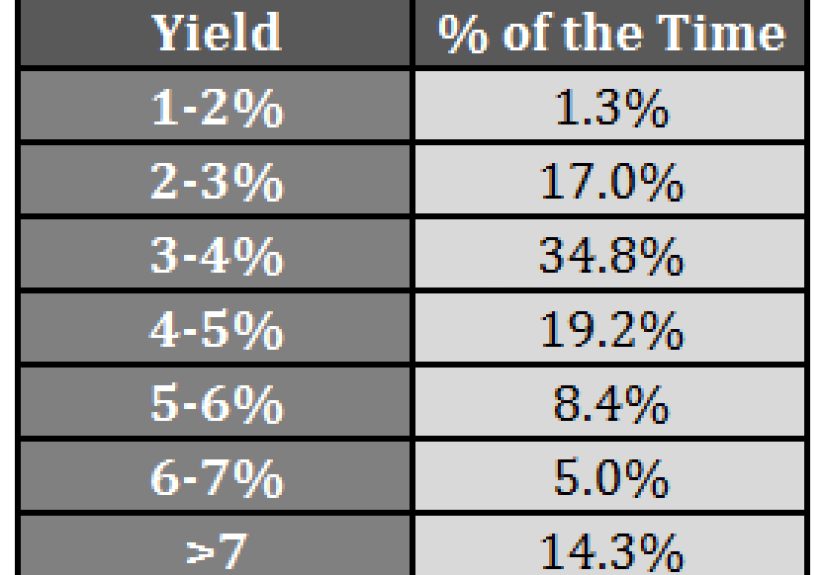

Valuations: Even “Average” Pricing Is Uncommon

One way investors try to define “normal” is valuationespecially the cyclically adjusted price-to-earnings ratio (CAPE),

popularized by Robert Shiller. The long-run CAPE average is often cited around the mid-teens. But the market doesn’t camp out there.

Historical data show it spends a relatively small share of time in a tight “normal” range.

Translation: the market is frequently either richer than “normal” (expensive) or cheaper than “normal” (a value investor’s love language).

If you’re waiting for the market to look perfectly average before you invest, you may be waiting long enough to qualify as a museum exhibit.

Returns: The Market Rarely Lands Near Its Long-Term Average

Long-term U.S. stock returns are often summarized as “about 10% a year” (give or take, and depending on time period and whether dividends are included).

The problem is that annual results don’t show up as “about 10%” very often. Some years roar. Some years sink.

Many years do something in betweenbut not neatly around the average.

This matters because investors tend to plan as if the market will behave like a metronome. It won’t.

The stock market is more like a drummer in a garage band: passionate, unpredictable, and occasionally loud enough to shake the garage door.

Volatility Isn’t a BugIt’s the Cover Charge

If markets were truly “normal,” investing would feel like collecting interest on a savings account. But stocks are volatile because uncertainty is the point:

you’re being compensated for taking risk. The price of that compensation is living through periods that feel uncomfortable.

Quick Definitions (Because Wall Street Loves Vocabulary)

- Pullback: A short-term dip (often loosely used for declines under 10%).

- Correction: Typically a decline of more than 10% but less than 20% from a recent peak.

- Bear market: Commonly a decline of 20% or more in a broad market index.

These labels are useful, but they can also mess with your head. Once a decline gets a scary name, it feels scarier.

(Nobody panics during a “minor adjustment.” Everybody panics during a “correction.” Same dip. Better branding.)

How Often Do Corrections and Bear Markets Show Up?

Historically, double-digit declines are not rare events. They’re recurring guests. Data compiled over long periods show many instances of 10%+ drops

and a meaningful number of 20%+ bear markets. The punchline is not that crashes never happenit’s that turbulence happens far more often than calm.

A practical way to think about it: if you stay invested for decades, you should assume you’ll experience multiple corrections, a handful of bear markets,

and at least one moment where you swear the market is personally attacking your retirement account.

Even “Good Years” Can Feel Bad Mid-Year

One of the most misunderstood parts of stock investing is that a year can end up positive while feeling awful in the middle.

In fact, the market often drops meaningfully at some point during the yeareven in years that finish with gains.

That’s not an exception. That’s the pattern.

Another underappreciated detail: even when the overall index looks calm, many individual stocks experience drawdowns along the way.

The index can be up, and a large share of its components can still have meaningful pullbacks. “Smooth index, bumpy ride” is more common than people realize.

If “Normal” Is Rare, What Should Investors Do?

The goal isn’t to find a normal market. The goal is to build a strategy that survives an abnormal onebecause that’s most of them.

1) Redefine Normal: Expect Discomfort in Exchange for Growth

A healthier definition of “normal market” is: “a market that regularly tests your patience.” If you can accept that,

you stop treating every decline like a surprise and start treating it like weather.

Not fun weather, necessarily. But predictable in its unpredictability.

2) Use an Asset Allocation You Can Live With (Not Just One That Looks Smart)

The best portfolio isn’t the one with the highest theoretical return. It’s the one you can stick with when headlines scream

and your group chat suddenly becomes a panel of macroeconomists.

- Diversify across stocks, bonds, and (if appropriate) other assets.

- Match risk to timeline: short-term goals shouldn’t depend on stock market mood swings.

- Plan for drawdowns: if a 20% decline would cause you to abandon the plan, the plan needs adjusting.

3) Don’t Confuse Activity With Progress

When markets get volatile, doing nothing feels irresponsible. That’s a human impulse, not an investing rule.

Often, the smartest move is boring: rebalance, keep contributing, keep costs low, and avoid emotional decisions.

The “Missing Best Days” Trap (a.k.a. Timing Is Expensive)

One reason markets feel so hard is that the worst days and best days tend to cluster.

Investors who jump out during scary periods risk missing the reboundsometimes the biggest gains happen shortly after the biggest drops.

Multiple major firms have published versions of the same lesson: being out of the market for only a handful of top-performing days

can dramatically reduce long-term results. The exact numbers depend on the time window studied, but the theme is consistent:

trying to sidestep volatility often means sidestepping returns.

The market doesn’t send you a calendar invite for the recovery. It just shows upsometimes while sentiment is still miserable.

That’s why “time in the market” tends to beat “timing the market” for most long-term investors.

Specific Examples of “Not Normal” That Are Actually Normal

Example 1: The Fast Drop (and Faster Emotional Overreaction)

Some sell-offs arrive quicklyprices fall, volatility spikes, and investors suddenly remember their risk tolerance was mostly theoretical.

These periods feel uniquely terrifying because they compress fear into a short time window.

Yet history shows sharp declines are part of equity investing, not proof the market is “broken.”

Example 2: The Slow Grind Down

Other downturns are slow: a series of disappointing months, grinding losses, and the mental exhaustion of “Are we there yet?” but for portfolios.

This version can be worse than a crash because it wears you down. You don’t panic onceyou simmer.

Example 3: The “Everything Bubble” Feeling

At various times, investors worry that valuations are too high, that a small group of mega-cap stocks is carrying the market,

or that optimism has become fragile. Sometimes those worries are justified. Sometimes they fade.

The point is that the market rarely feels perfectly safe, and waiting for perfect clarity is its own risk.

A Practical Playbook for When Markets Feel Weird

- Zoom out: Look at your timeline (5, 10, 20+ years) rather than your last 5 days of returns.

Short-term noise is loud; long-term compounding is quiet. - Check your plan, not the pundits: If your strategy is diversified and aligned with your goals,

it was designed for volatility. If it wasn’t, fix the structurenot the mood. - Rebalance with rules: Rules-based rebalancing can turn volatility into maintenance instead of melodrama.

- Keep contributing: Regular investing (like automated contributions) can help you buy through downturns without

needing to “feel brave” on command. - Control the controllables: costs, taxes (where applicable), diversification, and behavior.

You can’t control returns. You can control how much you pay and how often you panic.

None of this eliminates risk. It just keeps you from turning ordinary market chaos into permanent financial damage.

Investor Experiences: What “Normal” Really Feels Like (Extra Perspective)

Ask long-term investors what “normal” feels like, and you’ll rarely hear, “calm and predictable.”

You’ll hear stories about learning patience the hard wayand discovering that the market’s biggest tests are psychological, not mathematical.

A common experience goes like this: someone starts investing during a strong bull market. Their account rises, headlines feel optimistic,

and the “risk” part of “risk and return” seems mostly theoretical. Then the first real correction hits.

Suddenly, they discover the difference between knowing volatility exists and feeling it in real time.

Their brain begins producing extremely convincing arguments like:

“This time is different,” “I’ll get back in later,” and the classic, “I’m not panicking, I’m just being prudent.”

Another frequent experience: investors assume a diversified index fund will behave smoothly because it holds hundreds of companies.

Then they learn diversification doesn’t prevent declinesit prevents single-company disasters. The index can still drop 10%, 15%, or 20%.

Diversification helps you survive. It doesn’t help you sleep like a baby during turbulence.

(Babies sleep great. Adults check futures at 2:00 a.m. and call it “research.”)

Many investors also learn that “the market” and “my portfolio” can feel like two different planets.

An index might be flat for the year, while their holdings swing wildly depending on sector concentration,

international exposure, or a few high-volatility positions. This often leads to an important upgrade:

instead of chasing whatever just performed well, they start paying attention to portfolio construction,

position sizing, and whether their strategy is built for the next decadenot the next headline.

There’s also the experience of watching others react. In every volatile period, you’ll see:

the friend who sells everything, the coworker who suddenly becomes a day trader, and the relative who declares investing “rigged”

right before the market rebounds. Observing that cycle can be surprisingly helpful, because it reveals a quiet truth:

most damage comes from the decisions people make around volatility, not volatility itself.

Over time, seasoned investors often develop a different relationship with “not normal.”

They stop expecting calm. They expect the market to misbehave. They build emergency cash for real-life expenses,

keep risk assets for long-term goals, and treat downturns like a planned feature of the journey.

They may not enjoy corrections, but they’re less shocked by themand that reduces the odds of a portfolio-derailing overreaction.

The most useful takeaway from these shared experiences is simple:

you don’t have to predict the next market move to succeedyou have to build a plan that doesn’t require prediction.

Markets being “not normal” isn’t a sign you’re doing it wrong. It’s often just the price of admission to long-term growth.