Table of Contents >> Show >> Hide

- What Is Sequence of Return Risk, Really?

- Why Retirees Should Care More About the First 10 Years

- A Wealth of Common Sense: The Luck and Logic Behind Sequence Risk

- The Best Ways to Manage Sequence of Return Risk

- 1. Start With a Realistic, Flexible Withdrawal Rate

- 2. Diversify Beyond an All-Stock Portfolio

- 3. Rebalance IntelligentlyEspecially Around Withdrawals

- 4. Use a Cash or “Bucket” Strategy as a Shock Absorber

- 5. Consider a Rising Equity Glide Path

- 6. Build a Floor of Guaranteed Income

- 7. Stay Flexible: Spending, Work, and Expectations

- A Simple Common-Sense Checklist

- Real-World Experiences: What Managing Sequence of Return Risk Feels Like

- Bringing It All Together

Imagine you’ve finally retired. You’ve packed up your work laptop, said your goodbyes, and

ceremonially deleted your alarm clock app. The market has been kind for years, your portfolio

looks robust, and your spreadsheet says you’re good to go.

Then, in your first couple of retirement years, the market drops 30%… twice.

That gut-level panic you’re picturing? That’s what sequence of return risk is all about. It’s

not just how much your investments earn over time, but when they earn it

and that timing can make or break a retirement plan.

In this article, inspired by the common-sense approach made popular on the

“A Wealth of Common Sense” blog, we’ll walk through what sequence of return risk is, why it’s

such a big deal for retirees, and the most practical, research-backed ways to manage it without

turning your retirement into a full-time trading job.

What Is Sequence of Return Risk, Really?

Sequence of return risk is the risk that the order of your investment returns

will hurt you, even if the long-term average looks fine. When you’re accumulating savings,

bad years early on don’t matter that muchyou’re still adding new money, and future good years

can bail you out. But once you start withdrawing, the math flips.

Here’s the basic idea:

- Two retirees can earn the same average return over 20–30 years.

- One gets strong early returns and weak returns later.

- The other gets weak early returns and strong returns later.

- They withdraw the same amount each year.

The retiree hit with poor returns in the first decade may run uncomfortably low on money,

even though the spreadsheet says the long-term average return should have been “enough.”

The damage happens early, when the portfolio is largest and withdrawals are slicing into a

falling balance.

In other words, sequence of return risk is what happens when bad market timing collides

with fixed spending.

Why Retirees Should Care More About the First 10 Years

Research on withdrawal rates and historical market returns points to a harsh reality:

the first decade of retirement pulls a lot of weight. If those early years

deliver low or negative real (after-inflation) returns while you’re pulling money out,

your portfolio may never fully recover.

Think of your retirement timeline like flying an airplane:

-

Takeoff (the first 5–10 years) is where you face the most riskif something goes wrong here,

you don’t have much margin for error. - Cruising altitude (the middle years) is more forgiving if you’ve built in enough buffer.

-

Landing (later years) matters, but by then you’ve already seen how well the plan is working

and can adjust.

That’s why sequence of return risk gets so much attention in retirement planning. It’s not a

theoretical problemit’s the difference between “We’re taking the grandkids to Disney” and

“We’re cutting streaming services and couponing again.”

A Wealth of Common Sense: The Luck and Logic Behind Sequence Risk

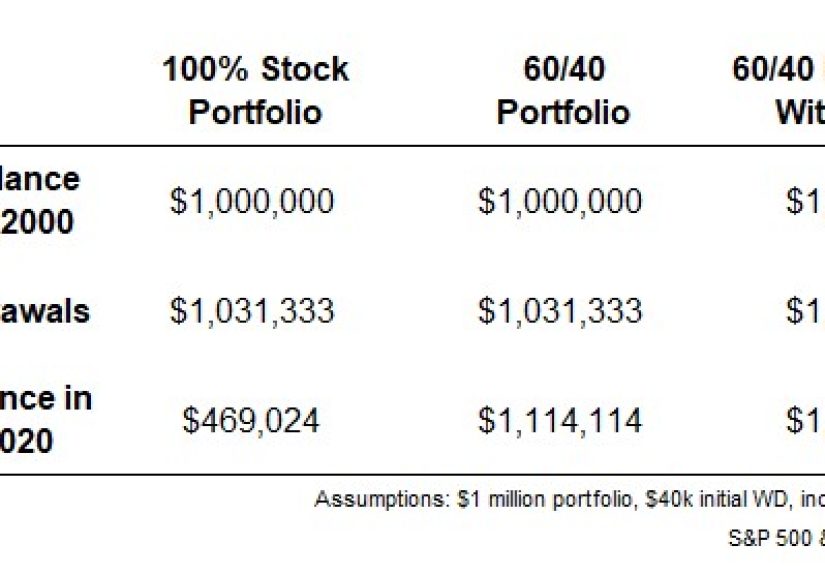

In his piece “The Best Way to Manage Sequence of Return Risk,” Ben Carlson uses a simple,

powerful example: a retiree with $1 million invested in the stock market who retires right

before a tough stretch of returns.

From 2000 to 2020, U.S. stocks returned a perfectly respectable average annual return.

But the early 2000s were roughthree down years right out of the gate. In Carlson’s example:

- The retiree starts with $1 million.

- They withdraw about 4% in the first year, adjusted each year for inflation.

-

With the “real” sequence of returns (bear market early), the ending balance is hundreds of

thousands of dollars lower than if those same returns had simply arrived in reverse order.

Same average return. Same withdrawals. Completely different outcomeall thanks to timing.

Carlson’s key takeaway is refreshingly down-to-earth: you can’t control market luck, but you

can blunt its impact with diversification, rebalancing, and a flexible financial

plan. Instead of trying to guess the perfect retirement date or “call” the top,

focus on building a portfolio and spending plan that can survive bad luck and take advantage

of good luck.

The Best Ways to Manage Sequence of Return Risk

1. Start With a Realistic, Flexible Withdrawal Rate

The famous “4% rule” says you can withdraw 4% of your portfolio in the first year of

retirement and adjust that dollar amount for inflation each year, with a decent chance your

money lasts 30 years. It’s a useful starting pointbut it’s not a guarantee, and it doesn’t

know what markets will do in your first decade.

Recent research and financial firms have suggested more conservative rates at times,

sometimes closer to the 3–3.5% range, especially when interest rates are low or valuations

are high. Some studies now point out that flexibility is more powerful than fixating on

a single “magic” percentage:

- Withdraw less in bad markets and give your portfolio breathing room.

- Allow yourself modest raises in good years instead of auto-inflation every year.

- Adjust for reality: health, taxes, and lifestyle all change over time.

A flexible withdrawal strategy can dramatically reduce the impact of a rough sequence of

returns without forcing you to live like a college student forever.

2. Diversify Beyond an All-Stock Portfolio

In Carlson’s analysis, the retiree who held a 60/40 mix of stocks and intermediate-term

bonds fared much better than the all-stock investor, even though bonds had lower returns

than stocks over the full period.

Why? Because bonds:

- Tend to fall lessor even riseduring equity bear markets.

- Provide a relatively stable source of cash for withdrawals.

- Smooth out the ride and reduce the emotional temptation to panic-sell.

Add in some international stocks, high-quality bonds, and maybe a bit of other diversifying

assets (like TIPS or certain alternatives), and you’ve got more than one lever to pull when

markets turn.

No, diversification won’t eliminate bear markets. But it can turn a portfolio-ender into a

portfolio headacheand that’s a meaningful upgrade.

3. Rebalance IntelligentlyEspecially Around Withdrawals

Rebalancing is one of those unglamorous investing chores that deserves way more credit.

When you rebalance, you:

- Sell a little of what has gone up.

- Buy a little of what has lagged.

- Bring your portfolio back in line with your long-term target mix.

During retirement, rebalancing also shapes where your withdrawals come from.

In good stock years, you can take more of your withdrawal from stocks and let your bonds

keep compounding. In bond-friendly years, you can lean more on bond income and leave your

stocks alone.

This “withdraw from the winner” approach quietly mitigates sequence risk by avoiding the

cardinal sin of retirement investing: selling deeply underwater assets just to fund living

expenses.

4. Use a Cash or “Bucket” Strategy as a Shock Absorber

One popular way to visualize sequence of return risk is with a “bucket strategy.” Instead

of viewing your retirement savings as one big blob of money, you divide it into time-based

buckets:

-

Bucket 1: Cash and short-term bonds (1–3 years of spending needs) to

cover near-term withdrawals without caring what the stock market is doing this week. -

Bucket 2: Intermediate-term investments (bonds, balanced funds) for the

next 3–10 years. -

Bucket 3: Long-term growth assets (stocks and other higher-return assets)

intended for 10+ years out.

In bad markets, you draw more from Buckets 1 and 2 and give Bucket 3 time to recover.

In strong markets, you refill the safer buckets by trimming gains from Bucket 3.

Whether you implement literal buckets or just keep a cash buffer plus a diversified portfolio,

the principle is the same: don’t let a temporary downturn force you into permanent losses.

5. Consider a Rising Equity Glide Path

A traditional “glide path” reduces stock exposure as you age. That makes sense when you’re

accumulating. But some research suggests that in retirement, a

rising equity glide path can actually lower sequence risk:

- Start retirement with a lower stock allocation.

- Gradually increase stock exposure over time.

The logic: you’re most vulnerable right after retirement, so it’s helpful to reduce risk

early. Later, once your portfolio has either survived or thrived, you can afford more equity

exposure to maintain purchasing power and handle longevity risk.

This isn’t for everyone, but it’s a good reminder that “set it and forget it forever”

isn’t the only option.

6. Build a Floor of Guaranteed Income

Another way to tame sequence risk is to make sure your essential expenseshousing,

basic healthcare, groceries, utilitiesaren’t fully at the mercy of the market.

That might mean:

- Maximizing Social Security benefits by delaying claiming if possible.

-

Using immediate or deferred income annuities to create a pension-like stream for core

spending. - Layering in other predictable income, such as rental income or part-time work.

Once the basics are covered by relatively stable income, your investment portfolio’s job

shifts from “fund every bill no matter what” to “fund lifestyle upgrades and long-term

flexibility.” That reduces the pressure to sell when markets are ugly.

7. Stay Flexible: Spending, Work, and Expectations

The common thread in most effective sequence-of-returns strategies isn’t some exotic product

or perfect formula. It’s flexibility.

People who navigate bad sequences well tend to:

- Trim nonessential spending in bear markets instead of pretending nothing has changed.

- Delay big-ticket items (new car, dream trip) when portfolios are temporarily depressed.

- Work part-time a bit longer if the timing of retirement coincides with a major downturn.

- Review their plan regularly with an advisor or at least a structured process.

This doesn’t mean you have to live in fear of the next crash. It just means acknowledging that

markets don’t care about your retirement dateand planning accordingly.

A Simple Common-Sense Checklist

If you want the “too long, didn’t panic” version, here’s a quick sequence-of-return

risk checklist you can discuss with a planner or work through on your own:

- ☑ Do I have at least 1–3 years of core expenses in cash or short-term safe assets?

- ☑ Is my portfolio diversified beyond just U.S. large-cap stocks?

- ☑ Do I have a rebalancing plan (e.g., once or twice a year, with clear rules)?

- ☑ Are my withdrawals flexible, or am I rigidly locked into a spending number?

- ☑ Are my essential expenses supported by fairly reliable income sources?

- ☑ Do I have a plan for what to do if the first 5–10 years of retirement are rough?

If you can honestly check off most of these, you’re already miles ahead of the “wing it and

hope” crowd.

Real-World Experiences: What Managing Sequence of Return Risk Feels Like

It’s one thing to analyze charts; it’s another to live through a nasty market early in

retirement. Let’s walk through a few realistic scenarios that bring sequence risk down

from the clouds.

Linda and Mark: The “Right Before the Bear Market” Retirees

Linda and Mark retire in what feels like a golden age: their portfolio has grown nicely,

interest rates are reasonable, and nothing in the headlines screams crisis. They’ve saved

$1.2 million, mostly in a balanced mix of stock and bond funds, and plan to withdraw 4%

in year one, adjusted for inflation.

Two years in, the market drops sharply. Their statement shows a six-figure decline,

and every news channel is talking about recession risk. This is where their plan matters.

Because they set aside two years of spending in cash and short-term bonds before retirement,

they’re not forced to sell stocks at the bottom. They temporarily pause inflation raises

in spending, skip the fancy kitchen remodel, and keep withdrawals flat for a couple of years.

Emotionally, it’s still stressful. But they’ve given their portfolio a fighting chance.

When markets recover, they rebalancetrimming some of the rebound from stocks to refill

their cash bucket. Ten years later, they’re still on track, and the 202X bear market is

just a story they tell their grandkids (the ones who still don’t understand what a bond is).

Carlos: Retiring Into a Bull Market

Carlos retires in a very different environment. The first five years are fantastic for

stocks. His diversified portfolio grows even as he pulls out 3.5%–4% per year. By year six,

he’s sitting on more money than when he retired.

Instead of assuming he’s a market genius, Carlos works with his advisor to adjust the plan:

- They modestly increase his fun spendingmore travel, more family experiences.

- They also lock in some gains by boosting his bond and cash buffers.

- They run new projections that show he can withstand a future tough decade without panic.

Carlos isn’t “beating” sequence of return risk; he’s recognizing that he’s temporarily on

the nice side of luck and using it to reinforce his long-term safety.

Dana and Lee: A Late-Career Course Correction

Dana and Lee planned to retire at 62. A market downturn at 59 rattles them, and their

projections suddenly look much tighter. Instead of stubbornly sticking to their original

date, they get practical:

- They push full retirement out by two years.

- They shift to a slightly lower-risk portfolio as they approach the new retirement date.

- They boost savings for a couple of years while markets recover.

Those two extra working years may not sound fun, but they dramatically improve the odds of

a stable retirement. They’re still retired for 25+ yearsbut now they’re less exposed to an

unlucky sequence right at the start.

These stories all share a theme: people don’t beat sequence of return risk with secret market

predictions. They manage it with buffers, flexibility, and a willingness to tweak their

plans as reality unfolds.

Bringing It All Together

Sequence of return risk isn’t about being pessimistic; it’s about being realistic.

You can’t control when bull or bear markets show up, but you can control:

- How concentrated or diversified your portfolio is.

- Whether you rebalance thoughtfully or let allocations drift.

- Whether you lock in income for your essentials or rely entirely on market swings.

- How flexible your withdrawal and spending habits are when things get rough.

The “best way” to manage sequence of return risk is not a fancy product or a complicated

formula. It’s a blend of common-sense stepsdiversify, rebalance, buffer, and stay flexible

wrapped inside a financial plan that accepts that luck, both good and bad, is part of the

journey.

That might not make for dramatic headlines, but it makes for a much calmer retirement.

And that, ultimately, is the whole point.