Table of Contents >> Show >> Hide

- Why “Both True” Thinking Is a Superpower in Investing

- Real Examples of Two Things That Are Both True

- 1) The consumer can be strong… and inflation can still hurt

- 2) Gas prices can feel outrageous… and still be historically “not that crazy”

- 3) The stock market can be “on a tear”… and still be average depending on the start date

- 4) Inflation can be scary year-over-year… and less scary when you widen the window

- 5) Tech can look unbeatable… and still be capable of getting wrecked

- 6) Inflation hedges can work beautifully… and fail right when you want them most

- 7) The market will crash again… and nobody gets a calendar invite

- 8) Markets can feel bubbly… and stay that way longer than you’d like

- The Practical “Both True” Framework for Real Investors

- A Few “Both True” Statements Worth Tape-Posting to Your Monitor

- Conclusion: The Calm That Comes from Admitting Complexity

- Experience Notes: of “Yep, That Happened” Moments (Composite Stories)

- SEO Tags

If you’ve ever stared at a market chart and thought, “This makes no sense,” congratulationsyou’re paying attention.

Money has a special talent for making smart people demand a single, clean, Hollywood-style plot twist:

either inflation is the villain or the economy is fine; either stocks are in a bubble or everything is rational; either you should buy now or you should wait for “the pullback.”

The problem is that investing doesn’t live in the land of “either/or.” It lives in the messier neighborhood of “both/and.”

And once you start thinking that way, a lot of investing stress stops being a mystery and starts being… normal.

Annoying, yes. But normal.

Ben Carlson at A Wealth of Common Sense nailed this idea in a simple format: “Two things that are both true.”

The brilliance isn’t in predicting the next CPI print or guessing the next market crashit’s in building the mental flexibility to hold competing truths without panic-selling your retirement plan.

Why “Both True” Thinking Is a Superpower in Investing

Your brain loves consistency. If inflation is high, then everything must be terrible. If the S&P 500 is near all-time highs, then a crash must be imminent.

If tech stocks have crushed it for years, then they must be “safe.”

That’s a comforting storybecause it gives you something to do. But markets punish simple stories.

“Both true” thinking does the opposite: it forces you to zoom out, change time horizons, and separate the emotional headline from the financial reality.

Real Examples of Two Things That Are Both True

The heart of Carlson’s post is that context changes everything. When you shift the timeframe, the same data can support two ideas that feel contradictorybut aren’t.

Here are the kinds of “both true” statements that show up in real life (and in your portfolio) all the time.

1) The consumer can be strong… and inflation can still hurt

In late 2021, it was possible for the U.S. consumer to look surprisingly healthyrising wages, high household net worth, and strong retirement balances

while inflation simultaneously ran hotter than most people had seen in decades.

Those facts don’t cancel each other out. They describe different parts of the same moment.

This matters because investors often treat “inflation is up” as a complete economic diagnosis.

But inflation is a symptom with many causes and many outcomes. It can squeeze budgets while household balance sheets remain resilient.

It can cool off later while asset prices keep moving.

2) Gas prices can feel outrageous… and still be historically “not that crazy”

Gas prices are the ultimate emotional index because they’re right there on a giant sign while you’re already annoyed.

In Carlson’s 2021 framing, prices could be dramatically higher than a year earlier while still below certain previous peaks (especially when adjusted for inflation).

The lesson isn’t “don’t complain about gas.” The lesson is: your most recent reference point will always feel like the only reference point.

Investors do this with everythinghome prices, stock returns, crypto charts, even grocery bills.

3) The stock market can be “on a tear”… and still be average depending on the start date

One of the sneakier truths in investing is that a decade can be incredible while a couple of decades can be merely okay.

That’s not a contradiction; it’s math plus timing.

If you measure from a major bottom, markets look unstoppable. If you include a nasty bear market (or two), returns suddenly look very normal.

The practical takeaway: you can’t build a plan around cherry-picked dates.

You build a plan around the assumption that your entry point will be “unfair” in some waytoo expensive, too scary, or both.

4) Inflation can be scary year-over-year… and less scary when you widen the window

The Consumer Price Index (CPI) measures inflation as experienced by consumers, based on changes in prices for a basket of goods and services.

When CPI spikes over a 12-month period, it feels like the floor just moved.

But longer windows can tell a more complete storyespecially if the prior year included unusual price declines.

This doesn’t mean inflation isn’t real. It means investors should be careful about letting a single timeframe become a permanent worldview.

Long-term financial decisions shouldn’t be driven by the emotional intensity of a single chart interval.

5) Tech can look unbeatable… and still be capable of getting wrecked

Every era has an “obvious” winner. The danger is when “obvious winner” mutates into “can’t lose.”

Tech has produced world-changing companies, and it has also delivered some historically brutal stretchesespecially when valuations got ahead of reality.

The point isn’t to fear technology. It’s to respect cycles.

Great innovations can be terrible investments if you pay the wrong priceor if you concentrate too much and confuse “my favorite sector” with “my entire plan.”

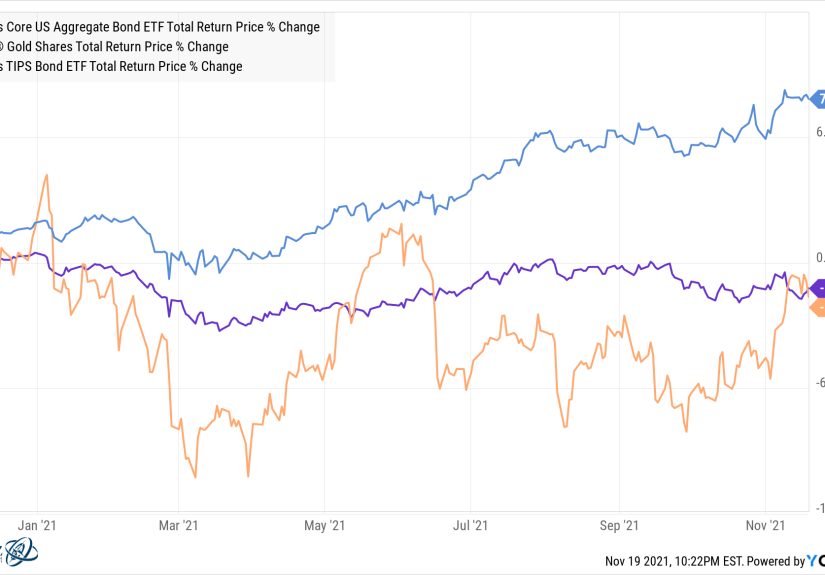

6) Inflation hedges can work beautifully… and fail right when you want them most

Investors love the idea of a perfect hedge: one asset that rises exactly when everything else is painful.

In practice, hedges are moody. Gold is a classic example: it had periods where it looked like an inflation-fighting hero, and other periods where inflation rose while gold disappointed.

Meanwhile, instruments designed specifically for inflation protectionlike Treasury Inflation-Protected Securities (TIPS)adjust principal with inflation and pay interest based on that adjusted principal.

That structure can make them behave more like what people wish their hedge would do.

Translation: “inflation hedge” doesn’t mean “always goes up when inflation goes up.”

It means “may help over certain regimes, with tradeoffs.”

7) The market will crash again… and nobody gets a calendar invite

Here’s the most honest pair of statements in finance:

the stock market will crash in the future, and nobody knows when or why.

You can be certain of the event and uncertain about everything that makes it tradable.

That’s why “prepare, don’t predict” is more than a slogan.

Preparing looks like diversification, sensible asset allocation, and enough liquidity to avoid selling at the worst moment.

Predicting looks like confident posts and expensive mistakes.

8) Markets can feel bubbly… and stay that way longer than you’d like

Feeling like something is overpriced is not the same as having a workable timing strategy.

Markets can be expensive, remain expensive, and still risebecause prices reflect expectations, liquidity, and human behavior, not just today’s fundamentals.

If your plan requires the market to “make sense” on your schedule, it’s not a planit’s a negotiation with reality.

Reality rarely countersigns.

The Practical “Both True” Framework for Real Investors

Holding two truths at once is nice in theory. But the real goal is to make better decisions when your emotions are screaming.

Here’s how to turn “both true” thinking into a portfolio habit.

Step 1: Decide what game you’re playing (months, years, decades)

Most investing stress comes from mixing time horizons.

If you need the money in six months, volatility is a genuine risk.

If you need it in twenty years, volatility is the entry fee.

Two things are both true: stocks are risky in the short run, and stocks have historically rewarded patient investors over long periods.

Your timeframe determines which truth matters more right now.

Step 2: Separate “my portfolio” from “the economy”

The economy is broad. Your portfolio is specific.

The economy can be ugly while markets rise.

The economy can look fine while markets fall.

Your portfolio should be built for your goals, not for winning debates about macro headlines.

Step 3: Diversify on purpose (not just “own a lot of stuff”)

Diversification is spreading investments among and within asset classes to manage risk.

It won’t prevent losses, and it won’t always feel brilliantbecause it means owning something that is underperforming at any given moment.

Two things are both true: diversification can reduce the damage of being wrong, and diversification can create the frustration of not being “maximally right.”

That frustration is the cost of durability.

Step 4: Use boring tools that beat dramatic instincts

- Dollar-cost averaging: investing at regular intervals can reduce the temptation to time the market.

- Rebalancing: periodically restoring your target allocation can force “buy low, sell high” behavior.

- Rules: written guidelines can stop you from freelancing during fear.

Two things are both true: dramatic decisions feel satisfying, and boring decisions often work better.

Step 5: Respect cash for what it is (and what it isn’t)

Cash is stability. It’s also a guarantee that inflation will slowly nibble your purchasing power over time.

Cash isn’t “bad.” It’s a tool.

It’s great for emergencies and near-term spending. It’s a lousy long-term growth engine.

Two things are both true: holding cash can help you sleep, and holding too much cash for too long can quietly sabotage your future.

A Few “Both True” Statements Worth Tape-Posting to Your Monitor

- The news can be alarming, and your plan can still be correct.

- Valuations matter, and they’re not a timing device.

- You can be early, and you can still be wrong for years.

- Inflation can spike, and long-term compounding can remain undefeated.

- Indexing can be simple, and sticking with it can be psychologically hard.

- It’s smart to learn about markets, and it’s dangerous to believe you control them.

Conclusion: The Calm That Comes from Admitting Complexity

The point of “Two Things That Are Both True” isn’t to sound clever at parties (although it can help).

The point is to stop treating uncertainty like a personal attack.

Markets will always give you mixed signals. Inflation can be up while parts of the economy hold up.

Stocks can be expensive while continuing to climb.

A crash is guaranteed, and the timing is unknowable.

When you accept that both sides can be true, you stop chasing the one perfect answerand you start building a plan that survives multiple realities.

That’s the kind of common sense that actually compounds.

Experience Notes: of “Yep, That Happened” Moments (Composite Stories)

The funny thing about “two things can be true” is that you don’t really learn it from a chartyou learn it from living through the parts where charts feel personal.

Below are composite, experience-based scenarios drawn from common investor anecdotes, coaching patterns, and the kind of mistakes people repeat because they’re human.

One classic moment: an investor watches the market hit new highs while inflation headlines dominate their feed.

They feel like it’s irresponsible to stay invested because “something has to give.”

Two things are both true: it’s reasonable to be uneasy about rising prices, and it’s also true that markets don’t wait for our comfort.

The investor sells “until things calm down.”

Then the market rises, and re-entry feels even scarier because now it’s higher.

They wanted safety; they got paralysis.

Another common experience happens with “the good performer.”

Someone’s portfolio is heavily tilted toward whatever has been winningoften a hot sector, a single mega-cap name, or the theme of the year.

They’re not trying to be reckless; they’re trying to be sensible.

The logic is simple: “Why own the laggards?”

Two things are both true: concentrating in winners can juice returns, and concentration can turn a normal drawdown into a personal financial crisis.

When the winner finally stumbles, the investor doesn’t just lose moneythey lose their narrative.

The real pain isn’t the decline; it’s the identity shift from “I’m a smart investor” to “maybe I just got lucky.”

Then there’s the “hedge heartbreak.”

People buy an inflation hedge expecting a straight-line relationship: inflation up, hedge up.

When that doesn’t happen, they feel tricked.

Two things are both true: some hedges can help over long periods, and any single hedge can disappoint over the exact window you care about most.

The mistake isn’t owning a hedge; it’s expecting a hedge to behave like a magic spell instead of a tool with tradeoffs.

The most relatable story is the one nobody brags about: doing the boring thing.

An investor keeps contributing through a scary year.

They rebalance when it feels uncomfortable.

They don’t “win” the year’s arguments on social media.

But over time, that consistency stacks up.

Two things are both true: it doesn’t feel heroic in the moment, and it often produces the best long-term result.

If you want the practical emotional takeaway, it’s this: feeling conflicted doesn’t mean you’re failing.

It often means you’re accurately perceiving complexity.

The goal isn’t to eliminate the discomfort. The goal is to keep the discomfort from driving the steering wheel.