Table of Contents >> Show >> Hide

- What People Really Mean When They Ask “Is This the Top?”

- Why Tops Are Easy to See in the Rearview Mirror

- 7 Signs You May Be Near a Top

- Different Tops Wear Different Outfits

- Famous Examples of Asking Too LateOr Too Early

- What to Do Instead of Trying to Nail the Exact Peak

- So, Is This the Top?

- Experience: What “Is This the Top?” Feels Like in Real Life

- Conclusion

Few questions create more drama, more sweaty palms, and more group-chat overreactions than this one: “Is this the top?” In investing, real estate, crypto, collectibles, and even hot business trends, that question usually pops up after prices have been climbing for a while and common sense has started to feel a little underdressed.

This article tackles the phrase the way most readers use it: as a question about whether a market, asset, or trend has reached a peak. And here is the slightly annoying but absolutely honest answer right up front: nobody knows for sure in real time. If calling exact tops were easy, Wall Street would be a calm place full of humble people, and we all know that is not how this movie ends.

Still, that does not mean the question is useless. Asking “Is this the top?” can be smart if it pushes you to look past hype and examine valuation, risk, concentration, credit, sentiment, and your own behavior. The goal is not to become a fortune-teller wearing a blazer. The goal is to make better decisions when excitement gets louder than evidence.

What People Really Mean When They Ask “Is This the Top?”

Most of the time, people are not asking for a precise timestamp. They are asking one of four things:

First, are prices too high relative to reality? In stocks, that might mean prices are running far ahead of earnings. In housing, it may mean homes cost much more relative to rents or incomes. In speculative assets, it may mean the story is huge but the cash flow is tiny, imaginary, or hiding under the couch.

Second, is enthusiasm becoming excessive? A rising market is normal. A market where everyone suddenly becomes an expert because they watched three short videos and downloaded an app at 1:14 a.m. is a different animal.

Third, is risk being underestimated? Tops often form when people stop asking what could go wrong and start talking as if gravity has been discontinued.

Fourth, should I do something different now? That is usually the real question. Sell? Rebalance? Wait? Panic? Not panic? Panic elegantly?

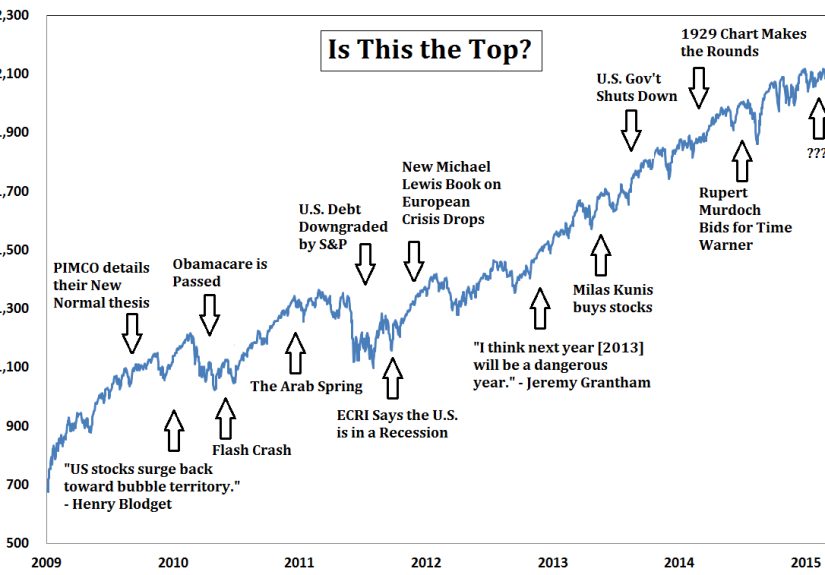

Why Tops Are Easy to See in the Rearview Mirror

A top does not come with a fire alarm. Prices can stay elevated for much longer than skeptical people expect. Strong assets can become expensive and keep rising. Weak assets can look absurdly overvalued and become even more absurd before reality finally shows up.

That is one reason experts warn against simple one-metric answers. High valuations can matter. Rapid price increases can matter. So can leverage, narratives, and speculation. But no single signal rings a bell and announces, “Congratulations, this was the final green candle.” Markets are messy because fundamentals, psychology, liquidity, and policy all collide at once.

Another problem is that some booms are partly justified. New technology can genuinely improve profits. Housing prices can rise because supply is constrained. A sector can dominate because the leading companies are actually very strong. The trouble begins when a reasonable story turns into a universal excuse for any price at all.

7 Signs You May Be Near a Top

1. Prices Start Outrunning Fundamentals

This is the classic warning sign. In stocks, investors often look at price-to-earnings ratios, long-term valuation measures, expected earnings growth, and whether revenue is actually supporting the excitement. In housing, economists often compare prices with rents and household incomes. In speculative markets, people ask the oldest question in finance: what cash flow, utility, or real-world value justifies the current price?

Important caveat: expensive does not automatically mean “about to crash.” It often means future returns may be lower, risk is higher, and disappointment becomes more dangerous. Think of it this way: high prices do not guarantee the party is ending tonight, but they do make the punch bowl look suspiciously shallow.

2. Market Leadership Gets Narrow

Late-stage booms often become concentrated. A handful of giant winners drag the whole market higher while the average asset is doing much less. That can be a sign of strength, but it can also mean the broader foundation is weaker than the headline number suggests.

When a market becomes top-heavy, investors need to ask whether they are still diversified or just holding the same story in several slightly different wrappers. A broad rally feels healthier than one where a few glamorous names do all the heavy lifting while everyone else is backstage pretending to clap.

3. Credit, Leverage, or Easy Money Fuel the Move

Many ugly busts were made worse by borrowing. When people use more leverage to chase rising prices, the upswing can accelerate, but so can the damage later. Credit-fueled booms are dangerous because falling prices do not simply reduce confidence; they can force selling.

This matters in stocks, private markets, real estate, and any environment where “buy now, sort it out later” becomes the dominant strategy. When people rely on cheap financing to justify aggressive risk-taking, a top gets more plausible.

4. The Narrative Gets Too Clean

Every bubble has a story. The internet will change everything. Housing never goes down nationally. This technology rewrites the economy. This asset class is the future. Sometimes the story is partly true, which is what makes it so powerful. But when the narrative becomes frictionless, skepticism disappears, and every objection is treated like a personality flaw, caution is usually warranted.

Stories drive markets because people do not buy spreadsheets; they buy futures they can imagine. The problem is that a great story can carry a terrible price.

5. FOMO Replaces Homework

One of the clearest late-cycle signs is behavioral, not mathematical. People stop asking, “What am I buying?” and start asking, “Why am I not already in?” That shift matters. It can lead to chasing hot stocks, speculative real estate, trendy sectors, and flashy digital assets with little regard for downside risk.

It is also the perfect environment for fraud. Scammers love urgency, social proof, celebrity vibes, and “can’t miss” language. If an opportunity is being sold like a once-in-a-lifetime deal that expires in six minutes, step away from the keyboard. Real value rarely needs a countdown clock with fireworks.

6. People Use Volatility Gauges Like Crystal Balls

Investors often look at sentiment indicators and volatility measures such as the VIX. These can be useful context tools. They can show complacency, fear, or changing expectations. But they are not exact top detectors.

Low volatility does not prove a market is safe. High volatility does not prove the top is in. These tools are best treated like weather reports: helpful, imperfect, and not a reason to build your entire house out of umbrellas.

7. “This Time Is Different” Becomes the Group Motto

Sometimes this time is different in some ways. New technology, new regulation, lower rates, tighter supply, and changing consumer behavior can all alter how markets behave. But when that phrase is used to dismiss every old lesson about valuation, cycles, or risk, it usually signals trouble.

A healthy market story can survive questions. A speculative one often gets offended by them.

Different Tops Wear Different Outfits

Not every peak looks the same. Stock market tops often involve stretched valuations, narrow leadership, and extreme optimism. Housing tops may show up through price-to-rent distortions, affordability breakdowns, and widespread beliefs that buying at any price is safer than waiting. Crypto or thematic booms often involve social media acceleration, celebrity promotion, and a rush into whatever sounds “next.”

Collectibles and alternative assets can behave similarly. Whether it is rare sneakers, art, watches, or trading cards, the same ingredients appear again and again: scarcity narratives, fast price appreciation, community hype, and buyers who increasingly view the asset not as something to own but as something to flip.

That is why the best version of the question is not simply “Is this the top?” It is “What kind of top might this be, and what is driving it?”

Famous Examples of Asking Too LateOr Too Early

The Dot-Com Bubble

In the late 1990s, internet-related companies captured enormous attention. The underlying technological shift was real and important. The pricing, however, often got detached from near-term business reality. Plenty of investors who were early in questioning valuations looked foolish for a while, because prices kept climbing. Then the bust arrived, and suddenly “boring fundamentals” looked much more attractive.

The Housing Bubble

The 2000s housing boom showed how dangerous narratives can become when mixed with credit. Price growth, flipping stories, loose assumptions, and easy financing created a cycle that felt unstoppable until it was not. Housing is especially tricky because people often blend investing logic with emotional logic. A home is shelter, status, identity, and leverage all wrapped into one expensive monthly payment.

Meme Stocks and Crypto Frenzies

More recent speculative episodes showed how fast narrative-driven assets can move when social media, mobile trading, and viral enthusiasm collide. Prices can surge far beyond traditional valuation frameworks for a while. That does not mean everyone involved is irrational. It does mean price action can become more about momentum and group behavior than durable value.

What to Do Instead of Trying to Nail the Exact Peak

If You’re a Long-Term Investor

Do not confuse caution with prediction. You do not need to call the top perfectly to act sensibly. Review your asset allocation. Rebalance if one part of your portfolio has become far larger than intended. Check whether your risk exposure still matches your goals. Add diversification where concentration has crept in. Continue investing according to a plan rather than according to whatever is trending before breakfast.

This approach may sound boring, but boring has an excellent long-term résumé.

If You’re an Active Trader or Speculator

Be brutally honest about what game you are playing. If you are trading momentum, own that. Use position sizing, exit rules, and risk limits. Do not suddenly pretend a speculative position is a “long-term investment” just because it went against you. That move is emotionally understandable and strategically terrible.

If You’re Buying a Home

Do not let national headlines do all the thinking for you. Housing is local. Ask whether the payment is affordable, how long you expect to stay, whether supply is tight, and whether rent comparisons make sense in your area. A house can be a bad short-term trade and still be a reasonable long-term lifestyle purchase. The reverse is also true.

So, Is This the Top?

Maybe. Maybe not. That is not a cop-out; it is the central reality. Tops are not identified with certainty in real time. What can be identified are conditions that make a top more likely: stretched prices, narrow leadership, heavy leverage, euphoric narratives, sloppy risk-taking, and widespread FOMO.

The smartest response is usually not all-in or all-out. It is to think in probabilities, not absolutes. If the evidence suggests risk is rising, act like risk is rising. Tighten process. Reduce concentration. Rebalance. Slow down. Ask harder questions. And remember that even wonderful assets can become lousy buys at the wrong price.

In other words, you do not need a trumpet blast announcing the top. You just need enough discipline not to confuse excitement with inevitability.

Experience: What “Is This the Top?” Feels Like in Real Life

The funny thing about asking “Is this the top?” is that it rarely feels academic in the moment. It feels personal. It shows up when your co-worker will not stop talking about a stock that doubled, when your cousin is suddenly a condo philosopher, or when your social feed is full of people using the word “generational” to describe something that did not exist 18 months ago.

One common experience is the fear of being late. You watch an asset rise and think, “I missed it.” Then it rises again and you think, “I really missed it.” By the third rally, your brain quietly replaces analysis with jealousy. That is when the question “Is this the top?” often becomes code for “Am I about to do something impulsive and call it strategy?” Many people buy not because they understand the asset better, but because they cannot stand watching others seem smarter, luckier, or richer.

Another experience is the opposite: the fear of selling too soon. Maybe you bought early, maybe you held through volatility, and now the gain is large enough to feel life-changing. Suddenly every decision feels dramatic. If you sell and it keeps rising, you will feel foolish. If you hold and it falls hard, you will feel greedy. This is where many investors learn that managing success can be harder than surviving losses. Winning creates its own kind of emotional chaos.

Homebuyers know a version of this too. You tour a house, lose a bidding war, watch prices rise, and begin to wonder if you should stretch your budget because “this is just the market now.” Then one month later the same house type looks even more expensive, and panic starts dressing itself up as practicality. Asking “Is this the top?” in housing often means, “Am I protecting my future, or am I freezing while affordability runs away from me?”

Then there is the experience of the person who ignored the hype entirely and still feels uneasy. Maybe they stayed diversified while everyone else chased the hot thing. They may have slept better, but they also watched neighbors brag at barbecues and online acquaintances post screenshots of eye-watering gains. The uncomfortable truth is that prudence can look stupid during the middle of a mania. That does not make it wrong.

The most useful personal lesson is this: the question works best when it is turned inward. Not “Is this the top?” but “What am I feeling, and what is that feeling tempting me to do?” Am I excited because the value is compelling, or because the crowd is loud? Am I holding because the thesis is intact, or because selling would hurt my ego? Am I buying a future or renting a fantasy?

That is where experience becomes wisdom. Over time, many people realize the real danger was never failing to call the exact top. It was letting the possibility of easy money rewrite their standards. Tops are dramatic, yes. But the bigger story is usually human behavior: impatience, envy, overconfidence, hope, and the eternal belief that this time, somehow, the escalator only goes up.

Conclusion

“Is this the top?” is a useful question only when it leads to better judgment, not theatrical forecasting. No indicator can tell you the exact moment a boom becomes a bust. But patterns do repeat. When price outruns fundamentals, concentration builds, credit expands, narratives harden, and FOMO replaces analysis, the odds of disappointment rise.

The wisest move is not to become obsessed with perfect timing. It is to build a process that can survive being early, late, or partially wrong. That means diversification, discipline, realistic expectations, and enough humility to admit that markets can stay irrational longer than your group chat can stay civilized.